The Ocean of Contradictions…

Central Bank of Tanzania in Background, with Tanzania Shilings in foreground

By TZ Business News Staff.

One report on Banking in Tanzania describes the sector as safe, stable and growing, A micro enterprise owner, or a Small or Medium Scale Enterprise (SME) owner reading the 2010 Ernst & Young Tanzania Banking Sector Performance Review might be convinced there is plenty of money out there available for use in Tanzanian businesses.

And yes, that view is correct. There is lots of money to go around for capitalizing worthy, eligible businesses in Tanzania, the Dar es Salaam Stock Exchange (DSE) Chief Executive Officer, Moremi Marwa re-affirmed the Ernst & Young report during a recent DSE media workshop in Dar es Salaam.

But the money market is riddled with contradictions and bottlenecks, casting a lot of doubt on the rosy reports. The donor funded Financial Sector Deepening Trust (FSDT) based in Dar es Salaam says of the Tanzanian situation: The inability of SMEs to access financing remains one of the most frequently cited constraints to business growth in the country.

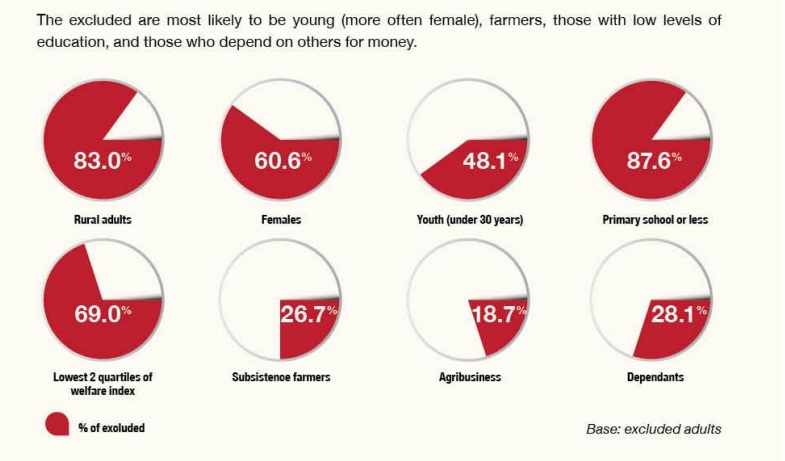

A survey conducted by the National Bureau of Statistics in collaboration with the financial services analysts FinScope found in 2013 that 83% of adult Tanzanians in need of financial services had no access to banking financial services, and that there were many barriers (problems) on both the services provision side and receiving end hindering access to finance.

Ernst & Young start their Tanzania Banking Sector Performance Review with the sector’s defiance of the world economic melt-down in 2008. Despite the financial crisis challenges arising that year, the Tanzania banking sector remained safe and stable all the way through 2009, the Ernst & Young report says.

In general, the sector is satisfactorily capitalized, with paid up capital recording an increase of 39%, (15% in 2008). The banking sector assets increased by 19% with the ratio of earning assets to total assets at 79% (83% in 2008).

The funding structure was mainly composed of deposits which increased by 24% and shareholders’ funds which increased by 28%. Furthermore, the banking liquidity is overall considered satisfactory, with the ratio of liquidity assets to deposits at 58% (54% in 2008).

Ernst & Young say they do not guarantee the accuracy of their data because their report is based on publicly published financial results audited or quarter four results as the only source of information, explaining that they realize there may be other undisclosed factors which may account for unknown bank performances, but the Tanzania banking sector is generally understood to be healthy.

Three banks entered the market in 2009: United Bank of Africa (UBA), Mkombozi Commercial Bank (Mkombozi), and Tanzania Women’s Bank (TWB). Furthermore, this year’s (2010) report has included the People’s Bank of Zanzibar (PBZ) and Tandahimba Community Bank (TCB) and prior years have been adjusted to include these two.

CRDB became listed in June 2009 at Dar es Salaam Stock Exchange. Also NIC Bank of Kenya acquired 51% of Savings & Finance Bank in September 2009 and in December 2009, I&M Bank Acquired 100% of CF Union Bank.

The Dar es Salaam Stock Exchange (DSE) Chief Executive Officer, Moremi Marwa told journalists during a stock exchange training workshop in Dar es Salaam recently he believed the Tanzania economy has a lot of money for businesses to use, but entrepreneurs do not get access to this money because they do not have bankable business plans — and nobody will finance a business which does not have a bankable plan.

Marwa encouraged SMEs to consider listing on the DSE to take advantage of the plenty of money available out there through the Enterprise Growth Market (EGM) window recently established at the DSE.

He said experience showed many initial publicly offered shares at the DSE (IPOs) were oversubscribed, proving there was a lot of money out there looking for good businesses in which to invest.

“There is enough liquidity to finance good, bankable projects,” Marwa told journalists. “People are sitting on money, but there is a general lack of awareness. We must anable well managed SMEs to also access capital from DSE.”

But the EGM at the Dar es Salaam bourse is meant for ‘strong’ SMEs. The window is meant to provide access to finance for SMEs with a capital base of at least Tsh. 200 million/-, making the DSE off limit to many cash strapped enterprises which comprise the majority of enterprises in the country.

FinScope Findings: Red Markers show majority of Tanzanians excluded from Financial services

There are approximately 3 million enterprises in Tanzania, with research indicating a large majority of these (98%) are family owned micro enterprises (employing less than 5 people), and located mainly in rural areas, according to the Economic and Social Research Foundation (ESRF).

The Dar es Salaam Stock Exchange is not likely to be useful to these enterprises any time soon.

Although data on the Micro, Small and Medium Enterprises (MSMEs) sector are rather sketchy and somehow unreliable, the figures reflect the SME sector wields an important role in the economy.

FinScope found out last year a mere 13.9% of adult Tanzanians with financial needs could get access to financial services, with another negligible percentage relying for the financial services from non-bank financial institutions such as mobile phone money transfer services where you cannot borrow for your business.

“Although there are now fifty different banks in the country—eleven more than in 2009—there is only a small rise in the total number of adults on both Zanzibar and the mainland who use bank products,”FinScope says in their latest report. “Those employed in agriculture are the least likely to use bank products and services, although access to mobile money has had a significant impact.”

Many of the estimated 3 million Micro, Small and Medium Enterprises (MSMEs) are rural based enterprises which operate informally.

While Moremi Marwa, of the Dar es Salaam Stock Exhange attributes lack of access to finance among Tanzanian entrepreneurs to lack of bankable business ideas, David Christian from the venture capital firm Haradali Capital gives a different explanation.

Talking to students at the University of Dar es Salaam Business School (UDBS) last year, the investment pundit said many Tanzanians—whether they be individuals or institutions were inherently risk averse and dividend driven.

Tanzanians will not put their money into anything they are not sure of getting dividends back. And this is what might explain the over-subscriptions of IPOs at the DSE. There is almost no risk out there.

FSDT has identified demand-side access to finance barriers in Tanzania as lack of verifiable borrower information or viable business plans, lack of collateral, absent or patchy record-keeping and a poor repayment culture among business owners.

But the trust has also identified problems on the supply side. The low access to finance is also widened by Tanzania’s “small number of banks with the interest or capability of serving SMEs and a low level of innovation leading to very limited offer in the range of appropriate products for financing SMEs.

“For instance commercial banks offer mainly deposit services and short term credit facilities. Facilities of three years and longer maturities are quite rare for SMEs. Based on our observations, there is almost no availability of supply chain finance products such as purchase order financing, invoice discounting, factoring or distribution finance, ” FSDT says. “ Also, other macro-level factors such as property and land ownership, regulatory requirements and the practices of securing loans affect bank behaviour and impose high transaction costs on SMEs.

“Other general challenges in SME finance in Tanzania relate to information gaps which fall into three categories: (i) knowledge of SME demand and market segmentation by financial institutions; (ii) SMEs knowledge of financial products in the market; (iii) financial literacy among SMEs.

FinScope identified the lack of education among entrepreneurs as a major bottleneck blocking access to finance, where the lack of education was on both financial matters and general education.

TZ Business News . Com conducted a random survey in Dar es Salaam last year and found another problem not identified by FSDT or FinScope: corruption blocks access to finance.

Cases were found in which a loan officer would ask an SME operator in need of say a Tsh. 10,000,000/- loan to borrow 12,000,000 in order to provide for a Tsh. 2,000,000/- bribe. An entrepreneur in need of Tsh. 10,000,000/- is thus forced to borrow an additional 2,000,000/- for corruption but which must be included in the loan.

The prospective borrower is therefore subjected to an added cost to the loan which might force him or her away from the bank loan, depending on the urgency of the financial need.