BUSINESS OPINION:

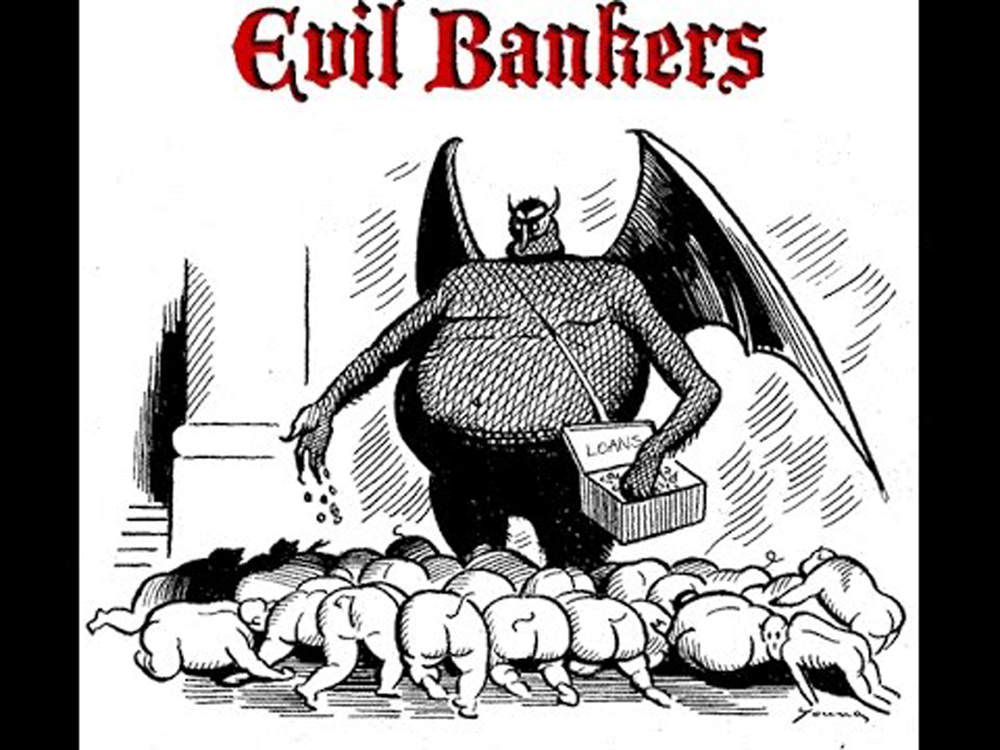

Banks are protected by the Credit Reference Bureaus. Customers should be protected from crooks in the banking sector by creation of a public Banking Services Customer Satisfaction Index.

By TZ Business News.

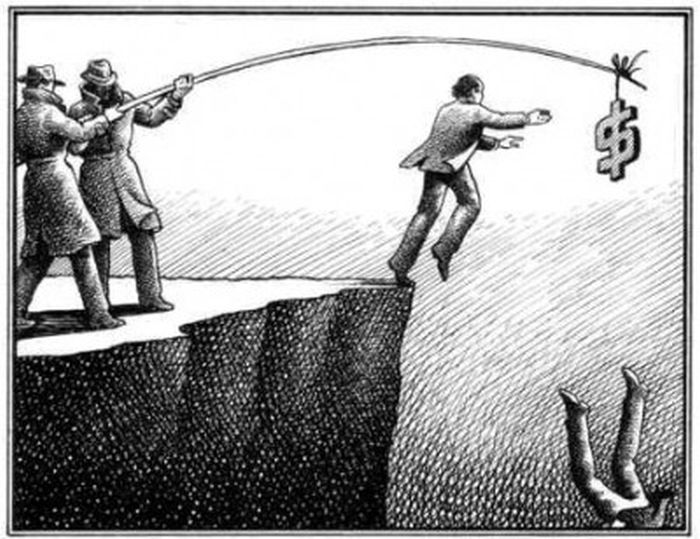

Efforts have been made in Tanzania to help banks identify ‘bad entrepreneurs’– or rather “bad debtors” as they are referred to among banks. And yes, bad debtors may exist among entrepreneurs in the Tanzanian business sector but bad banks exist too.

The Government has facilitated creation of a system to identify bad debtors. Two credit reference bureaus have been created for this purpose. Its not a bad idea at all, but this plan is terribly one sided in this website’s view. Something should be done about identification of bad banks where loan officers demand bribes from entrepreneurs seeking loans.

It is unfortunate the law which created Tanzania’s two Credit Reference Bureaus does not also force banks to sack loan officers who seek bribes from customers–particularly from struggling entrepreneurs in the SMEs where even the slightest disturbance in the cash flow can spell doom..

This opinion article is meant to explain how some bad debtors are actually created by corruption in the banks. The ultimate intention is to lead you into an understanding banks need to be exposed as a party to some bad debts. There are banks whose staff behave in ways that kill SMEs instead of building them.

It is against this backdrop that this website suggests financial services customers should consider forming a Banking Services Customer Satisfaction Index published annually to rate banks with the intention to lead bank users to better banks free of crooks. This customer satisfaction index should stand a good chance to expose corrupt elements in banks which contribute to creation of bad debts in the economy.

There are plenty of reported instances where loan officers and senior bank officials in various banks have solicited bribes from loan seekers. It is thus not unusual to find an entrepreneur in Tanzania complaining they wanted Tsh. 50 million to import goods from China but had to pay Tsh. 5 million as a kick-back to get the loan. Others may have wanted to ask for more to expand whatever it is they do. But the higher the demanded loan, the higher the kick-back loan officers may ask.

Many small SMEs in Tanzania do not insure their businesses. Now imagine what would happen if for some reason a planned business gets hit by a theft, or by some unforeseen political circumstance, or some natural disaster, or a market shift and the inventory can not be sold. The entrepreneurs will be forced to pay the principle loan plus interest for the entire amount taken from the bank, including the Tsh. 5 million kick-back. Loans are time sensitive. This can lead into loan defaulting which, consequently, can lead the businessman’s name into the bad books of the credit reference bureaus.

Reports from the financial markets this April, 2017 indicate credit to the private sector is low. What these reports are not saying is that there are business people who are not wanting to ask for loans from Tanzanian banks because they are afraid of problems which include corruption.

Who wants to lose a house or whatever collateral was used to get the loan because of loan defaulting where part of the money was actually squandered by some loan officer and his bank manager? I doubt anyone exists willing to accept such loss.

Go away with at least one important note from this opinion article; that for certain there are people in the business circles in Tanzania hesitating to borrow from banks because they want to keep away from crooks in the banking sector. Of course the prevailing dampened consumer spending atmosphere might be contributing to the current apparent hesitation to borrow as entrepreneurs fear an obvious slow movement of products, but bad behavior in the banks is a contributing factor.

Now the solution: two credit reference bureaus have been created in Tanzania to help banks identify bad debtors. This website proposes that need exists to ask the Tanzania Consumer Advocacy Society (TCAS) to establish a Banking Services Customer Satisfaction Index publishable each year to show by way of public opinion which bank to avoid.

The Tanzania Consumer Protection Act may exist alright, but what is an act of law without watchdogs and advocacy?

Banks are protected by the Credit Reference Bureaus. Customers should be protected from crooks in the banking sector by creation of a Banking Services Customer Satisfaction Index to warn people.

It is not true that every entrepreneur whose business goes under, or whose name ends up in the bad books of the Credit Reference Bureau is a bad business person. Some business people are just mere victims of a corrupt banking system.

A Banking Services Customer Satisfaction Index will go a long way in identifying bad banks. Developed countries learned many years ago a Customer Satisfaction Index is a very good way to censure bad service providers. The United States of America is a good example, where the American Customer Satisfaction Index (ACSI) is used as the national cross-industry measure of customer satisfaction.

This strategic economic indicator is based on customer evaluations of the quality of goods and services purchased in the United States and produced by domestic and foreign firms with substantial U.S. market shares. The ACSI measures the quality of economic output as a complement to traditional measures of the quantity of economic output.

The ACSI was started in the United States in 1994 by researchers at the University of Michigan, in conjunction with the American Society for Quality in Milwaukee, Wisconsin, and CFI Group in Ann Arbor, Michigan. The Index was developed to provide information on satisfaction with the quality of products and services available to consumers. Before the ACSI, no national measure of quality from the perspective of the user was available.

The ACSI model was derived from a model originally implemented in 1989 in Sweden called the Swedish Customer Satisfaction Barometer (SCSB). Claes Fornell, ACSI founder and Chair of ACSI LLC, developed the model and methodology for both the Swedish and American versions.

Hailed as the “Father of Customer Satisfaction,” Claes Fornell is without question one of the most influential scholars in marketing science today. His name can be found on 3 of the top 15 most academically cited papers from the leading sources in the field—Journal of Marketing, Journal of Marketing Research, Marketing Science, and Management Science.

The ACSI was first published in October 1994, with updates released each quarter. Starting in May 2010, ACSI data became available to the public on a more frequent basis, with results released multiple times per year. This change allows stakeholders to focus more in-depth on different segments of the economy over the entire calendar year. The national ACSI score continues to be updated quarterly on a rolling basis, factoring in data from 10 economic sectors and 43 industries.

The website Business Insider recently reported on the famous American food chain McDonald’s, whose slogan “I’m lovin’ it” was was found to be a lie because it did not necessarily ring true around the U.S.

The fast food chain earned the lowest customer satistaction score among limited-service restaurants, according to a recent report by the American Customer Satisfaction Index.

McDonald’s satisfaction rating is currently at 71, a 3% drop from last year. The average satisfaction rating for the survey is 80. The report is based on interviews with 4,572 customers chosen at random between January and March of this year.

They were asked about a range of benchmarks, including accuracy of order, courtesy of staff, quality of food, and menu variety. Smaller chains like Panera and Chipotle fall under ACSI’s “all others” category, which topped the ranking. According to the ACSI, Americans are turning to smaller chains for a better dining experience.

“In a weaker economy, consumers respond to price, but as the economy improves, quality becomes more important to restaurant customers,” Claes Fornell, ASCI chairman and founder, said in a statement. “This is good news for smaller chains and individual restaurants, which customers associate with higher food quality and better service.”

Now a final note to Bankers in Tanzania: Quit corruption!