Bank of Tanzania Director of Research and Economic Policy, Dr. Joseph Masawe

By TZ Business News Staff.

Efforts to bridge the income gap in Tanzania are bearing fruit, the Director of Economic Research and Policy at the Bank of Tanzania, Dr. Joseph Masawe said recently, explaining that Tanzania has reduced poverty by 18% during the last 14 years.

“If you look, out of 20 fastest growing countries in the world, actually 11 are from Africa, and three are in East Africa—Tanzania, Uganda and Rwanda,” Masawe said. “But the question we need to ask ourselves is whether this growth which we have realized in the past 10 years or so has been properly shared.” He made the remarks during the recent launch of the IMF Sub-Sahara African Economic Outlook Report in Dar es Salaam.

The government economist then added: “We have had complaints of good economic growth statistics but poverty not declining quick enough; but it is a bit gratifying to see that the recent household survey for Tanzania which was conducted recently shows that poverty is declining.

“If you look at the expenditure side of the households, we’ve been able to cut down poverty by about 18% between 2001 and now [2014],” he said.

The renowned Tanzanian economist, Professor Samuel Wangwe, had other views on the economic growth: “It is interesting that China growing at 7.5% is a real slow down and a concern. When here when we achieve 7.0% we say, oh, great!” he said during the discussions at the launch.

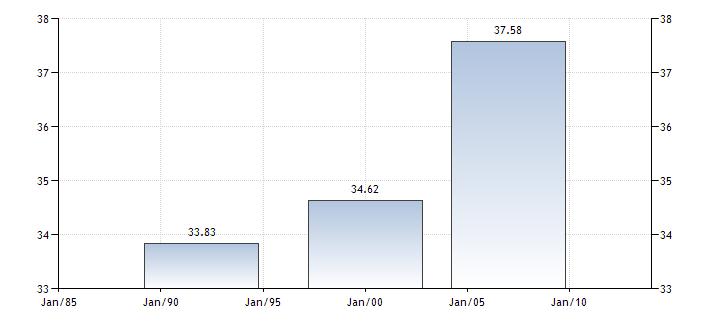

The World Bank income distribution fairness index, also called the GINI index for Tanzania, shows a measurement jump from 33 points in 1985 to 37.6 in 2013.The GINI Index is a scientific measure of fairness in the economy where a higher GINI index figure denotes increased unfairness on income distribution.

In June of 2014, the Tanzania Minister of Finance, Saada Salum Mkuya, told Parliament in Dodoma, central Tanzania, the country’s Real GDP was projected to grow by 7.2 percent in 2014 and to continue growing at an annual average of 7.7 percent in the medium term.

She also said the government planned to maintaining a single digit annual inflation rate whereby annual inflation rate for the period ending June 2014 was projected at 6.0 percent and 5.0 percent in June 2015.

“Households [in Tanzania] which own modern assets like cellphones, bicycles, radios has increased quite significantly over the period.” Dr. Masawe said. “I agree with the [IMF] report that actually we are growing quite fast…. There is clear evidence that we are growing fast. I think probably we are close now to take a strong position in the global economy to ensure that Africa contributes to global growth.”

Speaking during the launch, also, chairman of the Tanzania Bankers association, Dr. Charles Kimei, who is also Managing Director of CRDB Bank agreed the Tanzania economy was on the growth trajectory.

He however warned the central bank unrealistic interest rates might disturb lending to the private sector and therefore curtail economic growth. Financial policy mimicry of advanced economies would result in interest rates problems he said, adding that the central bank should adopt a realistic interest rate policy which takes into consideration the real situation that exists in the country.

It is a problem when the Central Bank increases capital adequacy ratios for commercial Banks, he said, giving one example. The rise of interest rates at the US Reserve Bank may also affect growth here because it may pose the danger of capital outflows as investors abandon the young African economies to go invest elsewhere where they are sure of the stability of the governments and the economies.

The IMF said in the report in October 2014 nations in East Africa and the rest of Sub-Sahara Africa will experience stronger economic growth in 2015 compared to 2014, if a number of risk factors can be contained.

Economics and Financial analysts Dr. Charles Kimei and renown economist Prof. Samuel Wangwe said the forecasted growth was possible, but they identified additional risk factors not seen by the IMF which could stifle the forecasted growth. The unseen risk factors include the problem of mimicking financial policies of advanced economies .

The Sub-Saharan Africa region’s economy was seen to grow by 5.1% in 2014 and was forecast to grow at 5.75% in 2015, Director of the African Department at the International Monetary Fund (IMF) in Washington, Antoinette Monsio Sayeh said at the launch of the October 2014 Sub-Sahara African Regional Economic Outlook report.

Countries in the East Africa sub-region are among the most robust economies in the Sub-Sahara Africa region, many of them growing at 5, 6 and 7 per cent this year, a robust pace which is expected to continue next year, she said, adding that the growth next year would be supported by continued public investment in infrastructure, a buoyant services sectors and strong agricultural production.

The economic slowdown in the Asian emerging markets, China and Europe may also weaken growth because these are the SSA region’s commodities export markets. A ‘disorderly’ normalization of the US monetary policy might also affect growth in the region.

Sub-Sahara Africa’s trade links with the world have increased dramatically during the past two decades, Sayeh Said. The economic situation in the other parts of the world therefore creates consequences in the region.

To mitigate risks, the IMF Director urged SSA countries to institute policies that enhance growth, with particular focus on boosting fiscal revenue mobilization, channeling spending towards infrastructure investment and other development needs while safeguarding social safety nets to encourage more inclusive growth. She also called on countries to improve the business climates, to focus on reducing inflation.

Discussing the report after the launch, Prof. Wangwe said it was certainly “a very informative report”. However, he said, the report encourages diversification of the economy during the forecasted growth, but it lacks clarity on what that diversification should mean.

“Moving from agriculture to services does not tell you very much whether agriculture itself is being transformed or whether the services themselves are the dynamic services,” he said. “The second issue it raises is whether this diversification, or strong growth is associated with moving from low productivity to higher productivity economic activity.”

The wish should be that the strong growth is associated with strong transformation, moving from low productivity activity to higher productivity activity, Prof. Wangwe said adding: “In the midst of this strong growth, the report suggests that policy should emphasize social safety nets in order to ensure ‘inclusive growth’. But we need to go beyond social safety nets, to make the growth involve broader participation in the growth itself, so that as the economy grows, it carries the majority of people with it.”

He said this growth lacks value. Inclusive growth should mean that the economy has broader participation in the growth process itself, creating jobs that are better remunerated, and that this should be the challenge in the next round.

The encouragement of exports should also focus on the exporting of value added exports, as opposed to the current situation in which “the majority of exports are predominantly primary commodities with very little value added indeed.”

The IMF has encouraged government to invest in infrastructure, but in this area public management should be addressed in that a way that the expenditures derive value. Many countries have high ‘per kilometer’ construction cost. Tanzania is one of the highest in the world, Prof. Wangwe said.

“So even if you put infrastructure, that raises the question: ‘couldn’t that be more cost effective?’ So we might be seeing growth but value for money challenges need to be addressed,” he said. “Cost effective public management. We should really go back into that.”

Dr. Kimei said the assumptions in the report will be useful to the banking industry because it provides information which shows how authorities and the central banks are likely to behave in terms of monetary policy since it talks about where fiscal policy should aim. The report also contains information which is likely to be relevant for much longer than the year 2014. “This is where we look to assemble our long term portfolio,” he said. “It is a good report for us. Although the report has emphasized on the downside, but there are many other factors that are mitigating those risks; especially if you are looking at one of two years to come. For example, the world market is currently experiencing a drop in oil prices,” he said.

“The decline in oil prices is going to release resources for use. It is going to create fiscal space, and that is going to mitigate the fiscal imbalance which have been cited. So I see the projection of a stronger growth is likely to happen,” he said. “It is likely to be even stronger despite the factors that work against the projected growth. I am an optimistic person. So I hope you don’t mind.”

From Left: Professor Samuel Wangwe, Dr. Joseph Masawe, Dr. Charles Kimei

Dr. Kimei said what he finds to be the bigger problem to work against growth in SSA will be the tighter global financial condition. “I think this is the more serious risk,” he said.

“Interest rates will rise on the world market. And with the rise of interest rates that might come with the change of policy at the American reserve bank, The Fed, and maybe Europe will be affected in a way. There would be a reverse of capital inflows,” he said. “And those reverse inflows may have very significant impact on the local market.”

The banker said the local market has speculative inflows which have come into Tanzania during the last five years, although unfortunately there was no data which would underpin the speculative flows. “I think that would be a very important piece of data to tell us that among the inflows that have been coming into the country in the last 2-3 years, which have come in the form of portfolio investment in the equities market in the stock exchange, some of it have gone out and borrowed.

“If interest rates go up there, they will want to go up there, they will take their money out of this country. This will lead to a very difficult situation for the authorities to manage the exchange rate,” Dr. Kimei said.

The interest rates turbulence would also affect investments in infrastructure in the region because it is mainly financed by sovereign bonds issuance, which means infrastructure is supported by foreign investors.

“When we talk about Public Public Partnership (PPP), who has capacity to go into PPP here, apart from pension funds maybe. The truth is that most of it expected to come from outside,” he said.

“The IMF Director has mentioned a link between sovereign bonds issuance and infrastructure financing…and I think the capital market has been very receptive because interest rates in Europe and America are very suppressed toward negative value in some cases,”Dr. Kimei said. “The capital market has looked to Africa and they have invested huge amounts as we see in Kenya and other [countries]. This money will now become very expensive.”

Another issue raised from the report is the need to expand credit to the private sector; that credit from banks to the private sector be increased.

“My fear is that credit to the private sector is going to decelerate because we are facing increasingly tight international financial stress, or distress—or whatever; we are now facing continued and tightened regulatory requirements. Capital adequacy ratios are being raised everywhere—not only here in Tanzania but even abroad.” The Banker said.

“If you increase capital adequacy ratio to around 15%, that is total capital to what you can make. That means where I could leverage my deposits 10 times when you have 15% you can only leverage 8%. And when you add your own buffer you can leverage only 5%; which means the possibility of banks to create credit is going to be reduced substantially. You can not grow when capital adequacy is very high,” Dr. Kimei said.

On this bank lending hindrance, the Banker said “of course you can understand the reasoning, but we have regimes that mimic the risks which are in developed counties. And if you look at the banks balance sheets here, the only risk is credit. There is no market for derivatives. It’s a simple market. My balanced sheet is loans and deposits and that’s it!”If you start having capital requirements for operations, for market risks, etc, etc, you constrain the resources, he said.