The exchange rate will be volatile, corporate bodies will shy away from bank borrowing. It confirms Tanzanians have less disposable income as the debt to disposable income ratio increases from 34.3 percent in September 2015 to 35.0 percent in March 2016.

Digital financial services providers have brought new risks. The Central Bank, in collaboration with other financial sector regulators will intensify surveillance.

By TZ Business News Staff.

The Bank of Tanzania (BoT) has confirmed International Monetary Fund (IMF) fears macro-economic risks face the Tanzania economy in 2016, pointing a finger at one particular possible cause—the volatile exchange rate which depends on interest rates in the United States of America.

The IMF sounded the warning in a statement issued a couple of days ago. The banking system is likely to be affected by the exchange rate volatility as corporate bodies shy away from Tanzanian bank loans in favour of other sources of financing, BoT says in its recent Financial Stability Report (FSR) signed by the BoT Governor, Prof. Benno Ndulu. BoT has also confirmed the widely held understanding Tanzanians have less disposable income in 2016.

The debt to disposable income ratio (proxied by the ratio of personal loan to employees’ compensation) increased from 34.3 percent in September 2015 to 35.0 percent in March 2016, the Bank says. But it may level off going forward. [An increase of the debt to income ratio means a family has less money to spend].

But the central bank argues in its report the Tanzania debt to disposable income ratio is however relatively low compared to other countries in the SADC region (South Africa 78.3 percent, Mauritius 79.0 percent and Namibia 76.2 percent).

Growth in household debt servicing cost ratio remained broadly unchanged. In the period ending March, 2016, the debt-servicing ratio increased to 10.4 percent from 10.1 percent in September, 2015. The debt servicing costs increased in conjunction with the rising share of personal loans in total bank loans and relatively high interest rates.

Nevertheless, BoT says, the banking sector remained sound as reflected by financial soundness indicators, but faced risk stemming from declining asset quality. In aggregate terms, capital and liquidity ratios remained above prudential requirements, at 18.0 percent and 36.6 percent against 12.5 percent and 20.0 percent, respectively except for few banks which require close monitoring. The risky banks are not identified.

The central bank has also reported that the asset quality declined in the banks during the six months under review as depicted by an increase in Non-Performing Loans (NPLs), which were 8.3 percent of total loans at end March 2016, compared with 6.8 percent in September 2015.

The NPLs were concentrated in credit extended to personal, agriculture and trade categories; all together constituted about 56.2 percent of the total NPLs at end March 2016 compared to 52.0 percent in September 2015.

Bank of Tanzania Governor, Prof. Benno Ndulu

The index measures dispersion of change. When above 50, although the ratio increased, overall sector’s capital buffer was sufficient to cover unexpected losses. The loan to deposit ratio has also increased to 82.7 percent at the end of March 2016 from 78.9 percent at end September 2015 matching the rapid private sector credit growth.

The developments have compelled some banks to pursue other funding options domestically and abroad, hence exposing them to interest and foreign exchange volatilities.

“The credit risk from households in the next six months is expected to remain broadly unchanged as banks take conservative lending stance to household,” the report says.

Prof. Ndulu says the Financial Stability Report (FSR) published every six months aims to create awareness about the vulnerabilities in the financial system and to inform the public about the resilience of the financial sector to stress.

The ultimate objective of a stable financial system is to support a vibrant and growing economy and to offer easy access to financial services across the country to all of its population, he says, adding that it is “a useful periodical health check of our financial system and I hope this issue once again provides useful information and guidance to all stakeholders.”

Since the release of the September 2015 FSR, global risks have been elevated with weaker growth prospects than earlier anticipated amid tighter financial conditions and lower commodity prices in the world.

Growth in Sub-Saharan Africa is vulnerable to sustained low commodity prices. Growth in the region is expected to slow-down to 3.0 percent in 2016 from 3.4 percent in 2015. This is partly attributable to low demand for imported raw materials by China which is undergoing structural transformation from manufacturing to a more services and high tech oriented economy, the report says.

The regional growth was further worsened by prolonged low global oil prices, mainly affecting oil exporting countries which account for about half of the region’s GDP. US Federal Reserve end of quantitative easing exposes some countries to capital flight, high cost of external borrowing and weakening of their currencies which may lead to build-up of public and private sector indebtedness.

The Tanzania economy was able to withstand risks on account of the diversified economy and beneficial effects of declining oil prices. Growth of the economy is expected to remain strong at 7.2 percent in 2016 compared with 7.0 percent in 2015, benefiting from its export diversity, government’s commitment to invest further in infrastructure and industrial development, and increased construction activity.

Inflation is projected to remain at single digits level, underpinned by favourable domestic food supply, subdued oil prices and prudent monetary policy.

Nevertheless, a weaker external environment and expected increase in interest rate in the USA may have spill-over effects on the economy through pressure on exchange rate and rising debt services for dollar denominated debt emanating from the Non-Financial Corporate (NFC) sector moderated due to decrease in foreign currency loans relative to equity, and increased use of internal financing as opposed to borrowing from the banking system.

Overall, the NFC Sector Survey conducted in December 2015 revealed that firms’ foreign currency denominated debt relative to equity declined while borrowing in local currency relative to equity increased. The outlook for NFC sector performance in the next 12 months is optimistic due to expected increased profitability and general business performance. This is confirmed by the increase in the overall performance sentiment index to 61.8 percent in 2015 from 46.6 percent in 2014.

Since firms are expected to enhance usage of internal financing as a result of expected increased profitability, potential risks to the banking sector from NFC borrowing will be lowered.

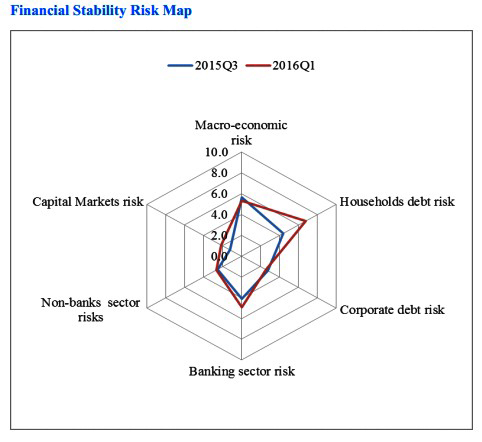

The risk emanating from global environment increased during the six months to March 2016, while risks arising from the domestic economy remained moderate. The global economy is exposed to uncertainties surrounding normalization of monetary policy in the US, and China rebalancing together with slowdown in growth.

As a result, global economic recovery remained sluggish, with volatile financial markets elevating potential risks to domestic financial system through exchange rate volatility and rising debt services on external borrowing.

Risks arising from the global financial environment are expected to increase on account of further tightening of the US monetary policy. This may trigger strengthening of US dollar against other currencies and create domestic financial markets volatility.

But the domestic economy is expected to remain strong despite persistent low commodity prices. The positive outlook is underpinned by diverse export base, declining oil prices and favourable macroeconomic environment.

Non-Performing Loans are expected to level off. This is based on the expectation that banks will enhance prudential risk management thus reducing the level of Non-Performing Loans in the banking sector. Risks arising from the corporate sector are expected to decline, as reflected by overall performance sentiment index. Total corporate leverage is expected to decrease in terms of domestic and foreign denominated debts.

Based on this outlook, the domestic financial system is expected to remain resilient in the next six months.

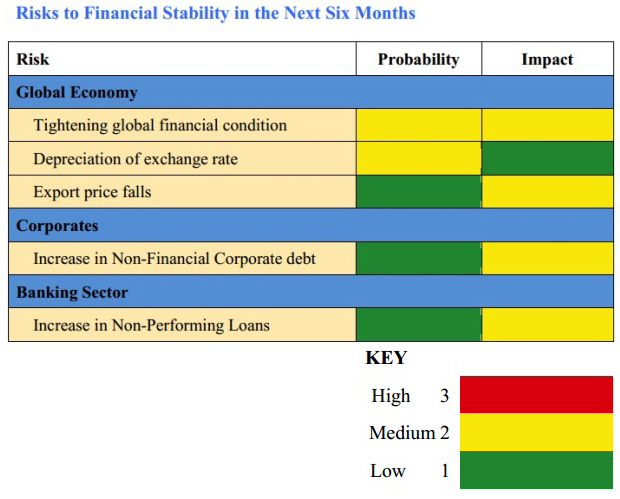

The banking sector was exposed to increased Non-Performing Loans mainly contributed by personal loans and loans to agricultural sector and trade. On the other hand, credit risks arising from the corporate sector were moderate. The identified risks are presented in the financial stability risk map below:

To minimize potential risks to the stability of the financial systems, the following recommendations are proposed. 1) Overall, NPLs to personal, agriculture and trade remained high, calling for close monitoring going forward. 2) Remain vigilant and take appropriate macro-prudential policy instruments mix to mitigate spill over effects of tight global financial conditions.

The Dar es Salaam Stock Exchange trading activity slowed down while share price indices recorded a decline. Total turnover for the quarter ending March 2016 was TZS 123.0 billion compared to TZS 220.0 billion recorded in September 2015. The decline is partly associated with normalization of markets after a period of high volumes traded following removal of capital controls to non-residents in May 2014.

In addition, All Shares Index declined by 3.9 percent on account of decline in profitability of some listed companies, leading to a fall in total market capitalization by 4.0 percent despite new listings. However, both the index and volume traded remained within long-term trend and do not signal any significant risk.

Insurance sector remained healthy as reflected by financial soundness indicators albeit declining profitability. The sector remained solvent with adequate liquidity and diversified investment portfolio. While investments in government securities and term deposits increased, investments in real estate declined in 2015 relative to 2014, implying a reduced risk exposure to the sector currently facing declining rental prices.

The change in the investment mix contributed to improvement in general and life insurers’ liquidity ratios which increased to 112.9 percent and 58.3 percent as at end December 2015 compared to 109.3 percent and 57.2 percent in the preceding year, respectively and both were within the prudential requirements.

Social Security Sector remained diversified, with increased membership albeit with a decline in Return on Investment. Generally, the sector complied with Investment Guidelines in terms of portfolio diversification. In addition, the sector attracted new membership from informal sector supported mobile money platform contributed to increase in new membership which grew by 9.0 percent to 2,345,869 in December 2015 from June 2015 Return on Investment declined to 2.1 percent from 4.8 percent in the same period.

The payment systems continued to operate with minimum disruptions and settlement risks. The volume and value transacted through Tanzania Interbank Settlement System (TISS) grew on account of increased usage by government agencies, financial institutions and individuals.

Despite increase in transactions the system maintained its server and database uptime availability of 100 percent and 98.3 percent, respectively. Meanwhile, during the period the Bank issued the Payment Systems Licensing and Approval Regulations, 2015 to allow for licencing and supervision of all payments services providers. This is expected to enhance regulatory oversight and mitigation of potential risks in the payments systems.

This gives explicit mandate to the Bank for licensing and supervision of all payment services providers, a major development in the financial system regulatory infrastructure considering the growing role of mobile money and other digital platforms in financial services delivery in the country. Going forward increased role of non-bank financial intermediaries and interaction between the financial system and the rest of the world may pose risk to the domestic financial system.

Accordingly, the Bank in collaboration with other financial sector regulators will intensify surveillance and expand macro-prudential toolkit in order to preserve the stability of the financial system.

The main risks to the stability of the domestic financial system in the next six months to September 2016 are summarized in the risk map. The risks are analysed and rated from low to high basing on their probability of occurrence, and the potential impact to domestic financial stability, should the risk build-up and materialize. Risks to Financial Stability in the Next Six Months: