Oil refinery

By TZ Business News Staff and Agencies.

If the price of oil determines the direction of a nation’s economy, then current information indicates it is safe to predict existing business trends will maintain their current pace.

Although Oil and gas markets can be highly volatile and opinions in the sector may change instantaneously and without notice, no major changes are expected on the price of oil in the next half of business year 2015.

Using data from four news agencies—the British Reuters, Iran’s Mehr, Russia’s Interfax and the French AFP, Radio Free Europe has quoted Iran’s oil minister predicting that OPEC is unlikely to cut oil output when the group of oil-exporting countries meets this coming early June.

Above: Iran’s Oil Minister Bijan Zanganeh. Bottom: Russian Energy Minister Aleksandr Novak .

“Lowering OPEC’s production ceiling requires consensus between all members,” Oil Minister Bijan Zanganeh was quoted as saying on May 24 by the semiofficial Mehr news agency. “Under current conditions, it seems unlikely that the OPEC production ceiling will change.”

Suggestions have been made ahead of the June 5 meeting that OPEC could cut production to boost flagging global oil prices. Saudi Arabia, one of the world’s leading oil producers, decided at the last OPEC meeting in November against cutting output.

Analysts expect the Gulf state to maintain the approach, which is intended to defend market share.

On May 23, Russian Energy Minister Aleksandr Novak said there was “no point” cutting global oil production, suggesting that demand will rise and the market will balance out if production and prices stay at the same level.

If the general trajectory of oil futures benchmarks over the past fortnight is anything to go by, it has yet again become quite clear that without a supply response, an oil price rally simply won’t materialize, Forbes Magazine reports.

Everyone from casual punters betting on a price rise to the most hardcore members of the long positions brigade have seen Brent and WTI front-month futures contracts creep up, not spike, marking a couple of notches upwards, only to retreat backwards.

The Forbes analyst says with authoritative aplomb, we were told by many commentators some months ago that US shale oil production would suffer in an era of low prices thereby triggering a supply correction, which in turn would bump up the price. If anything, that assertion has turned out to be a sweeping generalization applicable to some US shale plays (e.g. Bakken) but way off kilter for others (e.g. Eagle Ford).

Furthermore, any partial decline in output of US shale plays is being more than adequately met by an increase in production elsewhere, especially Saudi Arabia, Kuwait and the United Arab Emirate (UAE), as the International Energy Agency recently noted. In fact, Organization of the Petroleum Exporting Countries (OPEC), which is scheduled to revisit its production ceiling in June, is already pumping nearly a million barrels per day (bpd) above its official quota of 30 million bpd.

If you like your information to the decimal point, OPEC’s monthly oil report for April puts its members’ production at 30.93 million bpd to be exact. People often find conspiracy theories, but I have always believed in a Darwinian logicof a tussle for market share in a crude world where OPEC simply isn’t quite the swing producer it once was, despite having considerable clout.

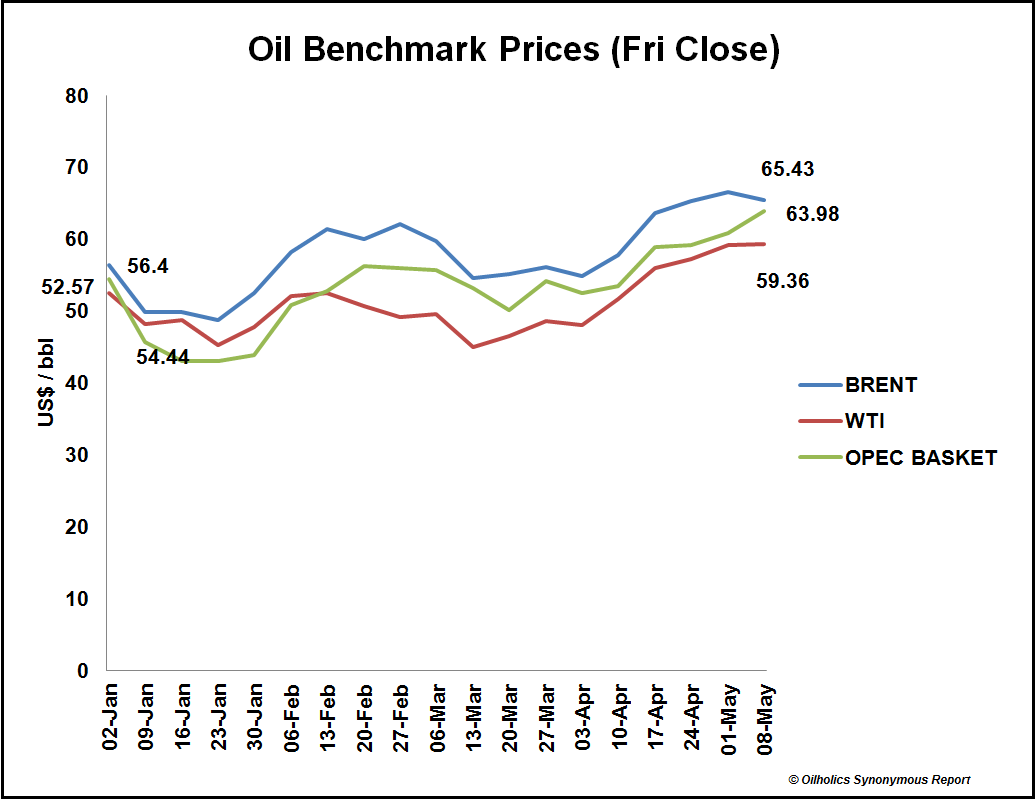

World oil price movement: Oil benchmark Friday closes 2 January to 8 May, 2015, using 21:30 GMT as a cut-off point © Oilholics Synonymous Report, May 2015 (Credit: Forbes Magazine)

Meanwhile, demand just isn’t firing up as nearly 1.3 million bpd of surplus oil keeps coming on the market. The said surplus is more than adequate to meet demands of the so-called “US driving season” and that of China, where every season used to be a driving season but the macroeconomic motor hasn’t been in fifth gear of late. Quite the contrary, for the last two quarters and counting, Chinese economic indicators have seen as many ups and downs as oil benchmarks.

Surplus oil means geopolitical risk, something most speculators going long often clutch on to, is not quite holding up. Tensions from Nigeria to Libya, Iraq to South Sudan continue unabated, but in the face of surplus oil volumes we are witnessing at the moment, the market is finding itself to be risk neutral, and will continue to do so barring a very serious geopolitical infraction or dip in oversupply to the 500k to 600k bpd range.

Ongoing Saudi intervention in Yemen offers a case in point. If what’s happening there, with indirect implications for oil and gas shipping via the maritime artery of Bab el-Mandeb Strait, would have transpired in 2011-12, we’d have a minimum of $5 per barrel oil price premium attributed to it. In 2015-16, it’s not quite turning out to be that way. Simply put, tragic as the events might be from a human standpoint, given the current oversupply scenario, many in the oil market don’t deem it to be a meaningful geopolitical development.

Collectively, all of this dumps both benchmarks in a $50 to $70 per barrel limbo range, equally dashing hopes of those predicting a drop below $30 and those suggesting we’d be at $100 in no time. [There are] reasons to believe benchmarks will be in this range for a while yet.

For starters, the global economy – led by China and the US – isn’t exactly in overdrive, but it isn’t materially worse either. A possible Greek default, should it happen won’t be a $30 oil price event. Bad as it might be, Greece won’t be a financial tsunami on the scale it would have been a couple of years ago when much of the European Union was caught unawares about the extent of the country’s systemic malaise.

Secondly, of the big five oil consumers – China, US, Japan, India and South Korea – only India’s demand is anything to write home about. Emerging market demand should go up steadily this year but won’t spike erratically, as empirical evidence points to refinery capacity utilization in many Asia Pacificmarkets not quite being what it used to be a mere 18 months ago.

Thirdly, an oil price remaining in the aforementioned range paradoxically doesn’t hurt very many major producers; especially US shale players. According to Wood McKenzie, US shale players need WTI prices to average at least $50 to maintain production level on a net basis. In March, [it was] noted from Houston, that some are managing to do so even at $35.

Finally, at current consumption levels, if a spike above $75 were to happen, it is bound to bring more oil on to the market serving as a drag on the price. Conversely, a sustained dip below $30 will cause a supply-side correction supporting price. [Neither can be seen] on the horizon.

One thing is certain, we’ve probably crossed the bottom of this cycle for Brent and that it should trade above $60 with a very gradual climb upwards. That is probably as far we would get with 2015 turning out to be predictably dull year.

In the absence of a breakthrough moment, be it a demand uptick or geopolitical flashpoint of global proportions; it is hard to see both benchmarks break free from their current ranges for better or worse. The so called supply-side correction will remain elusive over the next six months at the very least and without it we are more or less stuck in the range that we are in.